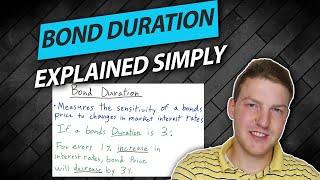

Fast Reader Notes: After completing this video, you should be able to: -Calculate the Macaulay The previous videos in this playlist have illustrated how we calculate the two most popular measures of single-factor interest rate ...

Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 - Knowledge Map

This page organizes Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 with clear context, related references, and useful follow-up topics while keeping the information easy to browse.

In addition, this page also connects Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 with for broader topic coverage.

Knowledge Map

The previous videos in this playlist have illustrated how we calculate the two most popular measures of single-factor interest rate ... After completing this video, you should be able to: -Calculate the Macaulay

General Reference Context

This part keeps Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 connected to practical references instead of leaving it as a single isolated phrase.

Topic Useful Tips

Before relying on any single result, compare related pages and verify important facts from stronger sources.

General Core Points

Important details can vary by source, so this page groups the most readable points into a scannable format.

Key points worth scanning

- After completing this video, you should be able to: -Calculate the Macaulay

- The previous videos in this playlist have illustrated how we calculate the two most popular measures of single-factor interest rate ...

What this page helps clarify

The main value is that it gives readers a lightweight hub for scanning and continuing research.

Helpful Questions

How does Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 connect to reference?

Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 can connect to reference when readers need context, examples, comparisons, or practical next steps inside the same topic area.

How does Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 connect to resource?

Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12 can connect to resource when readers need context, examples, comparisons, or practical next steps inside the same topic area.

What should be avoided when researching Applying Duration Convexity And Dv01 Frm Part 1 2025 Book 4 Chapter 12?

Avoid treating one short snippet as complete, especially when the topic involves money, health, law, schedules, or current details.